Why FinTech UX Design Is the Real Key to Faster SAMA & DFSA Approval

Most fintech founders think they have to choose between two things: a product that regulators approve, or a product that users actually want to use. Build for compliance, and you end up with clunky, text-heavy screens that kill conversion. Build for growth, and regulators flag your KYC flow, your disclosures, or your onboarding journey — sending you back to the drawing board. This is the trap that stalls fintech launches across lending, payments, neo-banking, BNPL, wallets, and investment platforms.

But it doesn’t have to be this way. The smartest fintech UX design doesn’t treat regulation as an obstacle to design around — it builds compliance directly into the user experience, turning transparency and clarity into trust signals that actually improve conversion.

The FinTech Launch Bottleneck Nobody Talks About

Here’s the pattern most fintech founders fall into: design the product, submit it to SAMA or DFSA, get rejected, redesign, resubmit, and wait another 4–6 weeks. Repeat that cycle two or three times, and a 3-month launch timeline quietly becomes 9 months or more.

Part of the problem is that there’s no shared playbook. Every founder ends up rebuilding KYC flows, consent screens, and transaction confirmation modals from scratch, with no documentation on what regulators are actually looking for. On top of that, most agencies outsource the compliance review to an external consultant, which adds weeks to an already long timeline and chips away at founder confidence right when speed matters most.

A Regulatory-Native Approach to FinTech UX

The alternative is what’s best described as regulatory-native UX design — designing into the constraints of SAMA, DFSA, and SCA requirements from day one, instead of treating them as a final compliance check before launch.

This works because of pattern recognition. After shipping 15+ regulated fintech apps, certain screens — KYC flows, consent journeys, transaction confirmations — start to follow patterns that regulators consistently approve. Designing with pre-vetted patterns means a product can be built once and submitted once, rather than redesigned after rejection.

Every design also ships with a regulatory checklist mapped against SAMA, DFSA, and SCA requirements, so founders know exactly which screens touch which regulation before anything goes to review. The result is a typical approval timeline of 2–3 weeks, compared to the industry norm of 8–12 weeks.

What makes this approach genuinely effective for growth, though, is the insight that the things regulators want — transparency, clarity, predictability — are the same things that build user trust. That trust is what drives loan acceptance, investment conviction, and BNPL approval rates upward, not downward.

Shariah-Compliant FinTech UX: Compliance as a Conversion Lever

Islamic fintech founders face a version of this same paradox, just with an added layer. Shariah requirements plus standard regulatory rules can easily push interfaces toward dense, text-heavy designs — the kind users don’t trust and regulators don’t find particularly polished either.

The fix is the same principle applied more deliberately: treat Shariah disclosure, contract clarity, and investment-source transparency not as friction to minimize, but as features that build user confidence. When fee structures, fund sources, and tax implications are made visible and clear upfront — rather than buried in fine print — users respond with more trust, not less. Compliance becomes differentiation rather than a tax on the experience.

This is where a strong fintech UX strategy and Shariah compliance genuinely reinforce each other instead of competing.

Why Arabic-First UX Design Matters for GCC FinTech

One of the most overlooked issues in Islamic and GCC-focused fintech products is localization. English-first design with an Arabic translation layered on top rarely converts the way founders expect. Saudi and Emirati users respond to interfaces that are culturally native from the wireframe stage — payment method defaults, social proof patterns, and even buyer psychology need to reflect local expectations, not be retrofitted after the fact.

Designing Arabic-first from the start, rather than translating after the English version ships, consistently produces better engagement and trust outcomes in GCC markets.

Proof in the Numbers: Real FinTech UX Outcomes

Two case studies illustrate how this approach plays out in practice.

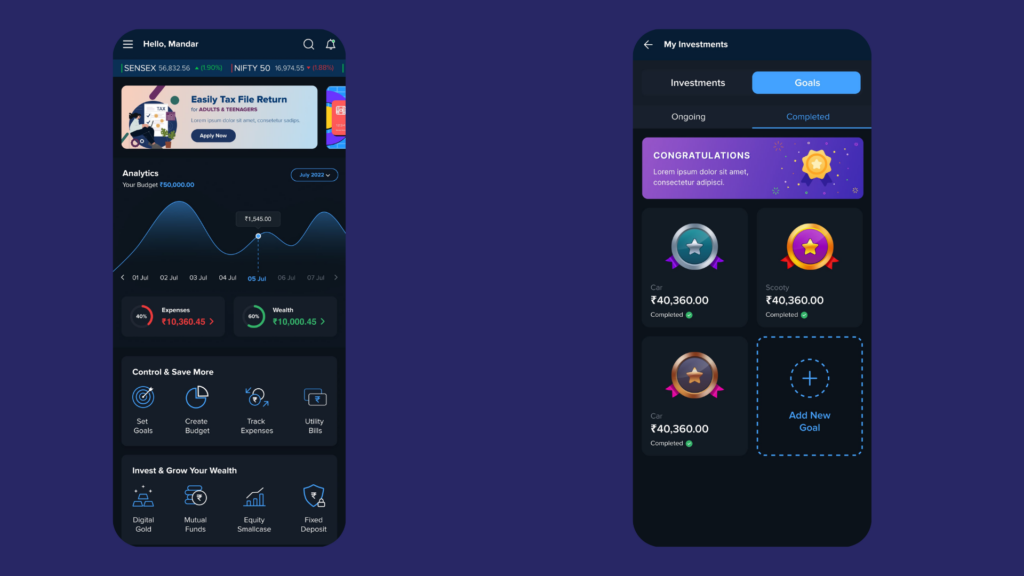

- Upwards (Lending): A digital lending platform with a complex KYC flow needed to balance RBI compliance with conversion. By switching to progressive KYC disclosure — revealing fields gradually instead of all at once — and being transparent about why each field was needed, the compliance screens became reassurance screens instead of friction points. The result: 40% faster loan applications, regulatory approval on the first submission, and a 35% increase in approval rates from fewer user drop-offs.

- FloatR (Wealth & SIP investing): This wealth platform targeted younger investors navigating fund selection, disclosure requirements, and tax implications — areas where the market average SIP conversion lift sits around 8–12%. By making fees, fund sources, and tax implications clearly visible upfront, transparency became the trust signal rather than the obstacle. SIP investment conversion rose by 45%, proving that users aren’t put off by clarity — they’re drawn to it.

Conclusion: FinTech UX Built on Trust, Not Trade-Offs

The biggest myth in fintech product design is that compliance and conversion sit on opposite ends of a spectrum. In reality, the regulatory requirements that protect users — clear disclosures, transparent fees, honest KYC flows — are the exact same elements that build the trust needed to convert them. Whether you’re building a conventional lending app or a Shariah-compliant investment platform for the GCC market, the fastest path to both SAMA/DFSA approval and strong user adoption is the same: design for transparency from day one. Founders who treat regulatory constraints as design inputs rather than design obstacles don’t just launch faster — they build fintech products users genuinely trust.